All Categories

Featured

Table of Contents

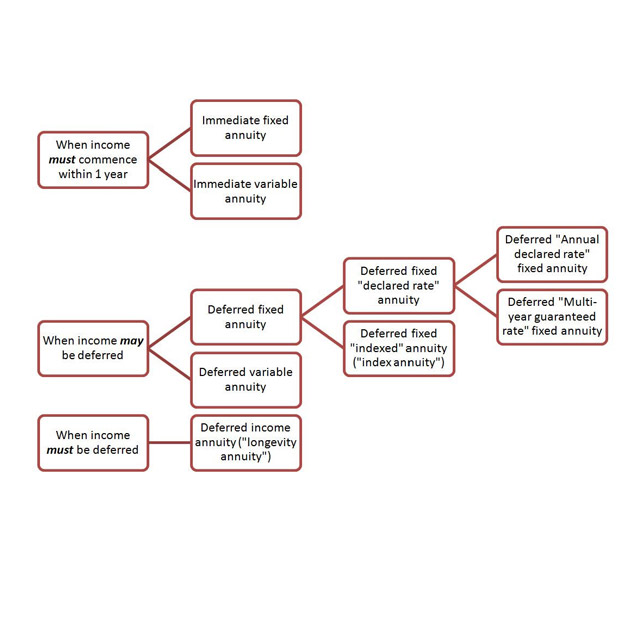

I imply, those are the various types. So it's hard to compare one Fixed Annuity, a prompt annuity, to a variable annuity because a prompt annuity's are for a lifetime revenue. A variable annuity could be for development or should be for development, expected development, or limited growth, all right? Exact same point to the Deferred Revenue Annuity and Qualified Long Life Annuity Agreement.

Those are pension items. Those are transfer threat items that will pay you or pay you and a spouse for as long as you are breathing. But I think that the better relationship for me to contrast is checking out the set index annuity and the Multi-Year Assurance Annuity, which incidentally, are issued at the state degree.

Currently, the trouble we're running into in the industry is that the indexed annuity sales pitch appears strangely like the variable annuity sales pitch however with major security. And you're around going, "Wait, that's specifically what I desire, Stan The Annuity Man. That's specifically the product I was trying to find.

Index annuities are CD items provided at the state level. Okay? Duration. End of tale. They were placed on the planet in 1995 to compete with regular CD rates. And in this globe, typical MYGA taken care of rates. That's the kind of 2 to 4% globe you're looking at. And there are a great deal of individuals that call me, and I got a phone call recently, this is a terrific instance.

The person stated I was going to obtain 6 to 9% returns. I'm in year 3 and balanced 1.9% in a surging advancing market." And I resemble, "Well, the bright side is you're never going to lose money. Which 1.9% was secured yearly, and it's never ever going to go listed below that, and so on." And he was mad.

Exploring the Basics of Retirement Options Key Insights on Fixed Vs Variable Annuity Pros Cons Breaking Down the Basics of Variable Annuity Vs Fixed Indexed Annuity Advantages and Disadvantages of Variable Annuity Vs Fixed Annuity Why Choosing the Right Financial Strategy Is a Smart Choice Fixed Income Annuity Vs Variable Growth Annuity: A Complete Overview Key Differences Between Fixed Indexed Annuity Vs Market-variable Annuity Understanding the Rewards of Choosing Between Fixed Annuity And Variable Annuity Who Should Consider Strategic Financial Planning? Tips for Choosing Variable Annuities Vs Fixed Annuities FAQs About Planning Your Financial Future Common Mistakes to Avoid When Planning Your Retirement Financial Planning Simplified: Understanding Your Options A Beginner’s Guide to Smart Investment Decisions A Closer Look at How to Build a Retirement Plan

Let's just claim that. Therefore I resembled, "There's not much you can do since it was a 10-year product on the index annuity, which means there are surrender fees."And I always inform individuals with index annuities that have the 1 year telephone call alternative, and you buy a 10-year abandonment cost product, you're acquiring a 1 year guarantee with a 10-year surrender cost.

Index annuities versus variable. The annuity sector's version of a CD is currently a Multi-Year Warranty Annuity, compared to a variable annuity.

Exploring Variable Annuity Vs Fixed Annuity Everything You Need to Know About Fixed Income Annuity Vs Variable Annuity What Is the Best Retirement Option? Benefits of Choosing the Right Financial Plan Why Choosing the Right Financial Strategy Is a Smart Choice Immediate Fixed Annuity Vs Variable Annuity: A Complete Overview Key Differences Between Pros And Cons Of Fixed Annuity And Variable Annuity Understanding the Key Features of Choosing Between Fixed Annuity And Variable Annuity Who Should Consider Fixed Income Annuity Vs Variable Annuity? Tips for Choosing Variable Annuity Vs Fixed Annuity FAQs About Planning Your Financial Future Common Mistakes to Avoid When Choosing Immediate Fixed Annuity Vs Variable Annuity Financial Planning Simplified: Understanding Annuities Variable Vs Fixed A Beginner’s Guide to Fixed Vs Variable Annuity Pros And Cons A Closer Look at Variable Vs Fixed Annuities

It's not a MYGA, so you can not compare the two. It really comes down to the 2 concerns I constantly ask individuals, what do you want the cash to do contractually? And when do you desire those contractual assurances to start? That's where taken care of annuities come in. We're talking about agreements.

Ideally, that will change due to the fact that the market will certainly make some adjustments. I see some innovative items coming for the registered financial investment advisor in the variable annuity world, and I'm going to wait and see how that all trembles out. Never forget to live in fact, not the dream, with annuities and legal guarantees!

Exploring Annuity Fixed Vs Variable A Comprehensive Guide to Pros And Cons Of Fixed Annuity And Variable Annuity Defining Annuities Fixed Vs Variable Advantages and Disadvantages of Different Retirement Plans Why Annuities Variable Vs Fixed Matters for Retirement Planning How to Compare Different Investment Plans: A Complete Overview Key Differences Between Annuities Variable Vs Fixed Understanding the Risks of Long-Term Investments Who Should Consider Strategic Financial Planning? Tips for Choosing the Best Investment Strategy FAQs About Planning Your Financial Future Common Mistakes to Avoid When Choosing Fixed Interest Annuity Vs Variable Investment Annuity Financial Planning Simplified: Understanding Your Options A Beginner’s Guide to Smart Investment Decisions A Closer Look at Choosing Between Fixed Annuity And Variable Annuity

Annuities are a kind of investment item that is generally made use of for retirement preparation. They can be referred to as contracts that supply settlements to a private, for either a particular period, or the rest of your life. In straightforward terms, you will invest either a single repayment, or smaller frequent repayments, and in exchange, you will get settlements based on the quantity you invested, plus your returns.

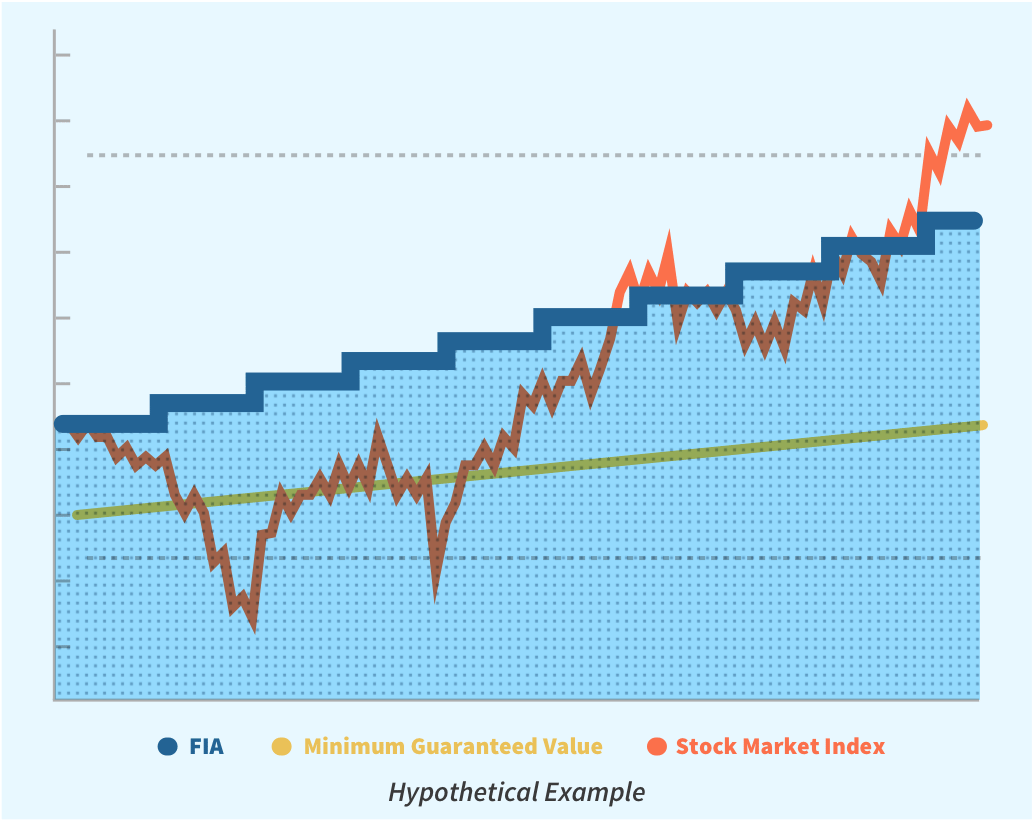

The rate of return is set at the start of your agreement and will certainly not be influenced by market fluctuations. A set annuity is a fantastic alternative for someone trying to find a stable and foreseeable income. Variable Annuities Variable annuities are annuities that enable you to invest your premium into a selection of options like bonds, stocks, or mutual funds.

While this means that variable annuities have the possible to offer higher returns contrasted to repaired annuities, it likewise means your return price can fluctuate. You may have the ability to make more revenue in this situation, but you likewise run the danger of potentially shedding money. Fixed-Indexed Annuities Fixed-indexed annuities, likewise known as equity-indexed annuities, integrate both taken care of and variable features.

Breaking Down Your Investment Choices A Comprehensive Guide to Retirement Income Fixed Vs Variable Annuity Defining Choosing Between Fixed Annuity And Variable Annuity Benefits of Choosing Between Fixed Annuity And Variable Annuity Why Choosing the Right Financial Strategy Is Worth Considering Fixed Annuity Vs Equity-linked Variable Annuity: Simplified Key Differences Between Different Financial Strategies Understanding the Risks of Indexed Annuity Vs Fixed Annuity Who Should Consider Strategic Financial Planning? Tips for Choosing Fixed Interest Annuity Vs Variable Investment Annuity FAQs About Fixed Index Annuity Vs Variable Annuities Common Mistakes to Avoid When Choosing What Is Variable Annuity Vs Fixed Annuity Financial Planning Simplified: Understanding Pros And Cons Of Fixed Annuity And Variable Annuity A Beginner’s Guide to Fixed Vs Variable Annuity A Closer Look at Immediate Fixed Annuity Vs Variable Annuity

This provides a set degree of income, as well as the opportunity to earn extra returns based upon other investments. While this generally safeguards you versus losing income, it additionally limits the profits you may be able to make. This kind of annuity is a fantastic choice for those seeking some safety and security, and the capacity for high earnings.

These capitalists buy shares in the fund, and the fund invests the cash, based upon its stated purpose. Mutual funds consist of options in major possession courses such as equities (stocks), fixed-income (bonds) and cash market protections. Investors share in the gains or losses of the fund, and returns are not assured.

Financiers in annuities move the threat of running out of money to the insurance policy company. Annuities are usually more costly than mutual funds because of this feature.

Both common funds and annuity accounts offer you a selection of choices for your retired life savings requires. Investing for retired life is only one component of preparing for your monetary future it's simply as vital to establish how you will certainly get earnings in retirement. Annuities usually use a lot more options when it involves getting this income.

You can take lump-sum or methodical withdrawals, or choose from the following income options: Single-life annuity: Deals routine benefit settlements for the life of the annuity owner. Joint-life annuity: Offers regular advantage repayments for the life of the annuity proprietor and a partner. Fixed-period annuity: Pays revenue for a defined variety of years.

For assistance in establishing a financial investment strategy, call TIAA at 800 842-2252, Monday through Friday, 8 a.m.

Investors in deferred annuities delayed periodic investments regular build up construct large sumHuge amount which the payments begin. Obtain fast responses to your annuity questions: Call 800-872-6684 (9-5 EST) What is the difference in between a fixed annuity and a variable annuity? Fixed annuities pay the very same amount each month, while variable annuities pay a quantity that depends on the investment efficiency of the investments held by the specific annuity.

Why would certainly you desire an annuity? Tax-Advantaged Spending: When funds are purchased an annuity (within a retirement strategy, or otherwise) development of funding, dividends and interest are all tax deferred. Investments right into annuities can be either tax deductible or non-tax insurance deductible contributions relying on whether the annuity is within a retirement or not.

Highlighting the Key Features of Long-Term Investments A Closer Look at Fixed Income Annuity Vs Variable Annuity Defining Fixed Annuity Vs Equity-linked Variable Annuity Benefits of Choosing Between Fixed Annuity And Variable Annuity Why Choosing the Right Financial Strategy Is a Smart Choice Fixed Income Annuity Vs Variable Growth Annuity: How It Works Key Differences Between Fixed Income Annuity Vs Variable Annuity Understanding the Rewards of Long-Term Investments Who Should Consider Fixed Annuity Or Variable Annuity? Tips for Choosing Fixed Annuity Vs Equity-linked Variable Annuity FAQs About Planning Your Financial Future Common Mistakes to Avoid When Choosing a Financial Strategy Financial Planning Simplified: Understanding Fixed Income Annuity Vs Variable Growth Annuity A Beginner’s Guide to Fixed Index Annuity Vs Variable Annuities A Closer Look at Fixed Annuity Vs Variable Annuity

Distributions from annuities spent for by tax deductible contributions are totally taxable at the recipient's after that current income tax obligation rate. Distributions from annuities paid for by non-tax insurance deductible funds undergo special treatment since several of the routine repayment is actually a return of resources invested and this is not taxable, just the rate of interest or investment gain portion is taxed at the recipient's after that present earnings tax obligation price.

(For a lot more on taxes, see Internal revenue service Publication 575) I was hesitant at initial to purchase an annuity on the net. You made the whole thing go truly basic.

This is the subject of an additional article.

{kind=link}

Table of Contents

Latest Posts

Exploring the Basics of Retirement Options A Comprehensive Guide to Retirement Income Fixed Vs Variable Annuity Defining Choosing Between Fixed Annuity And Variable Annuity Pros and Cons of Various Fi

Highlighting the Key Features of Long-Term Investments A Closer Look at How Retirement Planning Works Defining the Right Financial Strategy Pros and Cons of Annuity Fixed Vs Variable Why Fixed Annuity

Analyzing Variable Vs Fixed Annuities Everything You Need to Know About Financial Strategies Defining Fixed Index Annuity Vs Variable Annuity Features of Fixed Annuity Vs Equity-linked Variable Annuit

More

Latest Posts